One gram of gold,

five ways to hold it.

Buy it, earn yield on it, borrow against it, tokenize it, and redeem it for the physical bar — on one ledger, across four markets, at a published spread of 1.5% or less.

Fiveproducts,fusedononestack.

Most apps stop at buy and sell. Aadigo turns a single vaulted gram into a financial primitive — and unifies the whole life cycle under one identity and one double-entry ledger.

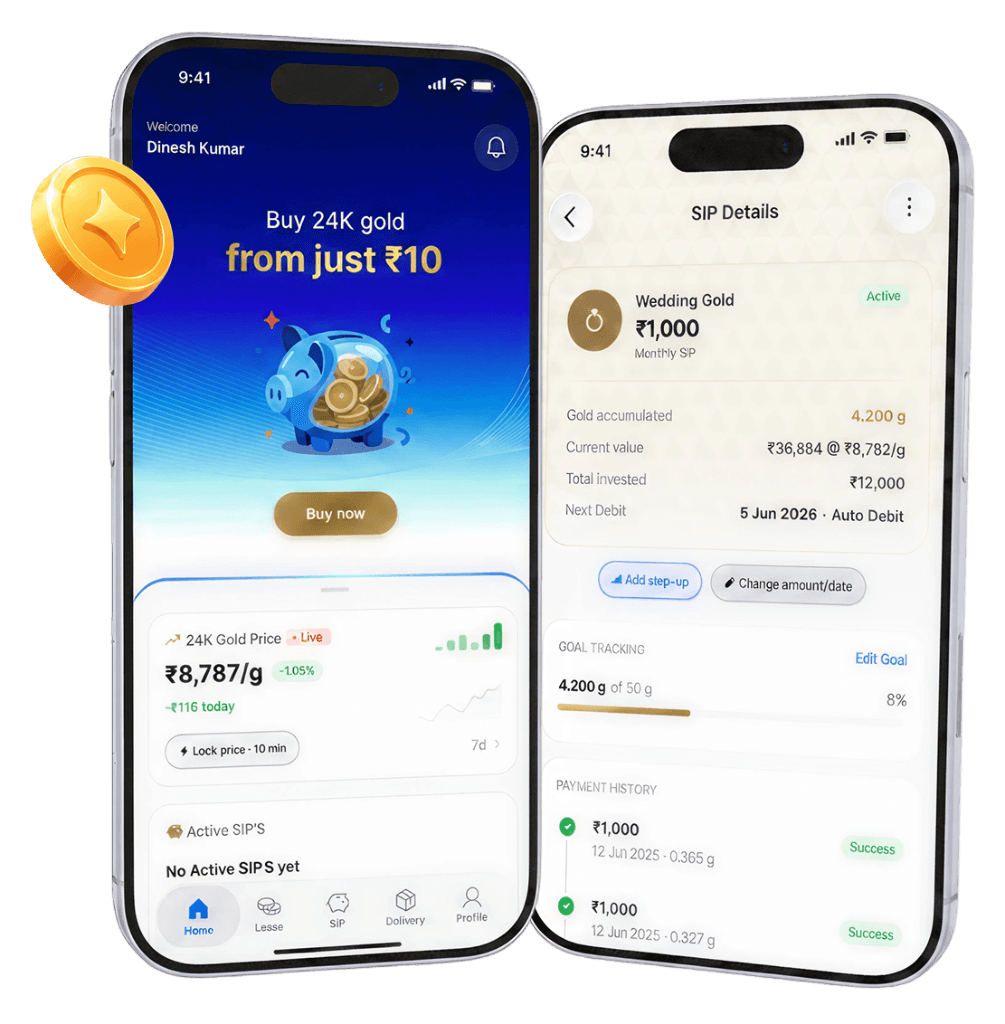

The on-ramp

Digital Gold

Fractional 24K from ₹10. Real-time LBMA pricing, auto-invest by UPI / GIRO / QRIS, gifting and joint holdings.

Earn — yield

Gold Lease

Opt in to lease stored gold and earn 3–5% p.a., paid in additional grams or fiat. Insured, audited, 7-day notice.

Borrow — instant credit

Gold Loan · xLoan

Pledge digital or physical gold for credit at up to 75% LTV, disbursed to UPI or e-wallet in minutes.

The cross-border layer

Tokenized Gold · xAU

On-chain gold under ERC-3643 — identity-gated, backed 1:1, Chainlink Proof-of-Reserve verified, redeemable at any partner store.

Fiat & crypto

Multi-rail Funding

Buy with INR, SGD, MYR, IDR, or major crypto like USDC and USDT, auto-converted via regulated OTC and travel-rule rails.

Closing the loop

Redemption Network

Reserve, scan a store QR, walk out with the bar. Once 500+ jewellers are live across four markets, the network is the moat.

The same gram, five lives — no bullion shipped.

A student in Coimbatore buys it. Her family puts it to work and pledges it. Her uncle in Singapore holds it as a regulated token. Her cousin in Jakarta walks into a counter and takes it home.

Buys ₹10 of gold

Fractional 24K, vaulted with a SEBI-regulated custodian, backed 1:1.

Earns yield on it

Leased to the bullion partner at 3–5% p.a., still insured and audited.

Pledged for credit

Her mother borrows instantly against it at 75% LTV via a partner NBFC.

Held as a token

Her uncle holds the same gram as xAU — a regulated, on-chain claim.

Redeemed at a counter

Her cousin scans a QR at a PT Pegadaian store and collects the bar.

Oneidentity.Oneledger.Andeachofthemchargedlessthanincumbentschargeforanysingleoneofthosethings.

Best spread in market — and healthy unit economics.

“Charge less” alone fails. Aadigo makes the buy/sell spread a loss leader and earns across loan, lease, FX, redemption and B2B instead of front-loading everything onto the spread.

All-in spread, indicative · lower is better

Revenue is diversified, so the visible price can be lowest while the business stays profitable. The actual profit centers sit elsewhere:

The leaders have scale.

They do not have depth.

India finally has a compliance perimeter. Indonesia's carve-out makes the loan unusually accessible. Singapore's GOLDX proved the architecture — and left retail untouched. The window is open.